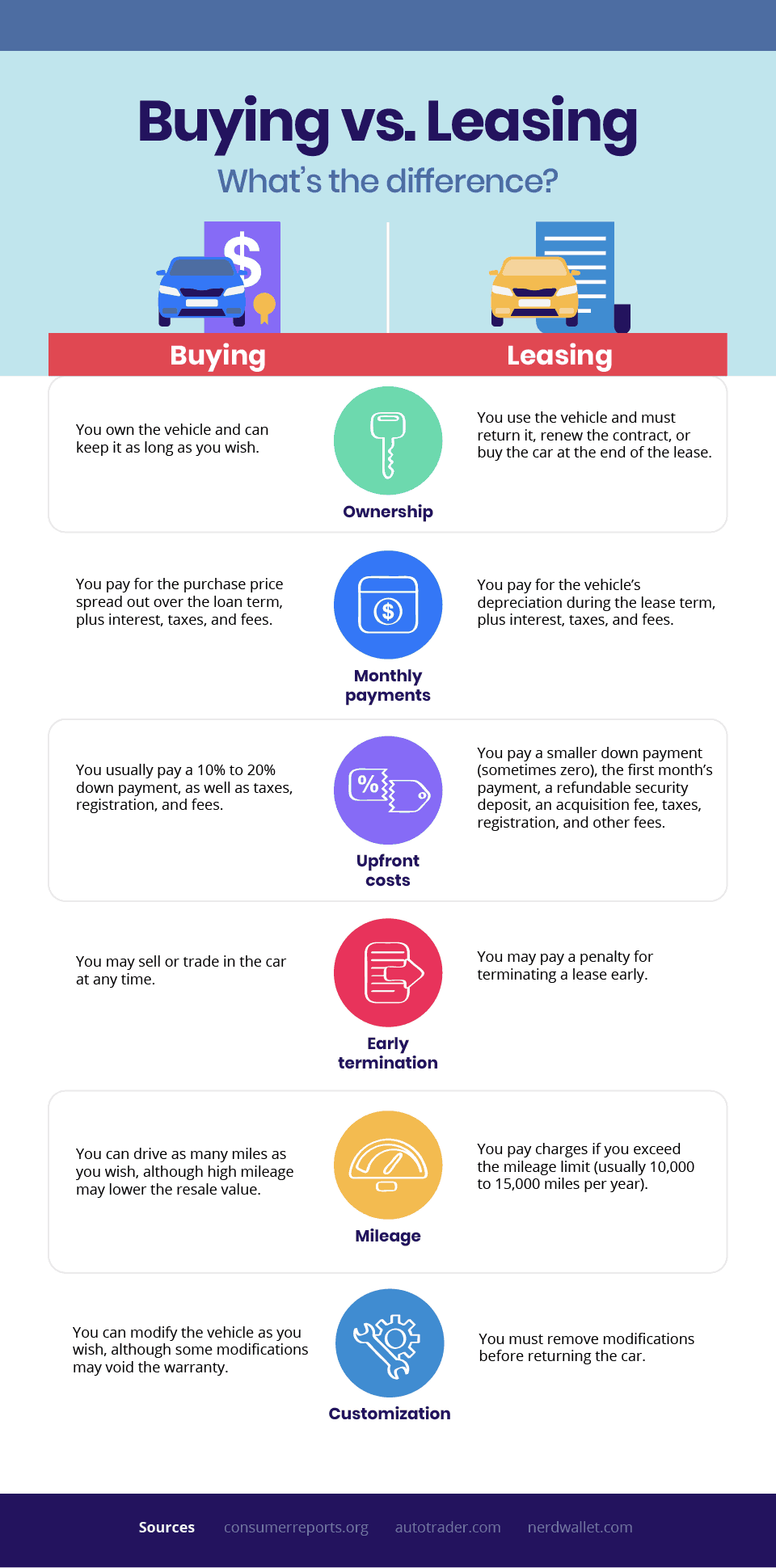

Are you ready for a new set of wheels? A vehicle is a large expense for most families. Recently, more people are choosing to lease their new ride instead of buy it; nearly 30 percent of new car transactions are leased. Keep reading to discover the pros and cons of buying versus leasing and decide which is right for you.

When It’s Better to Buy

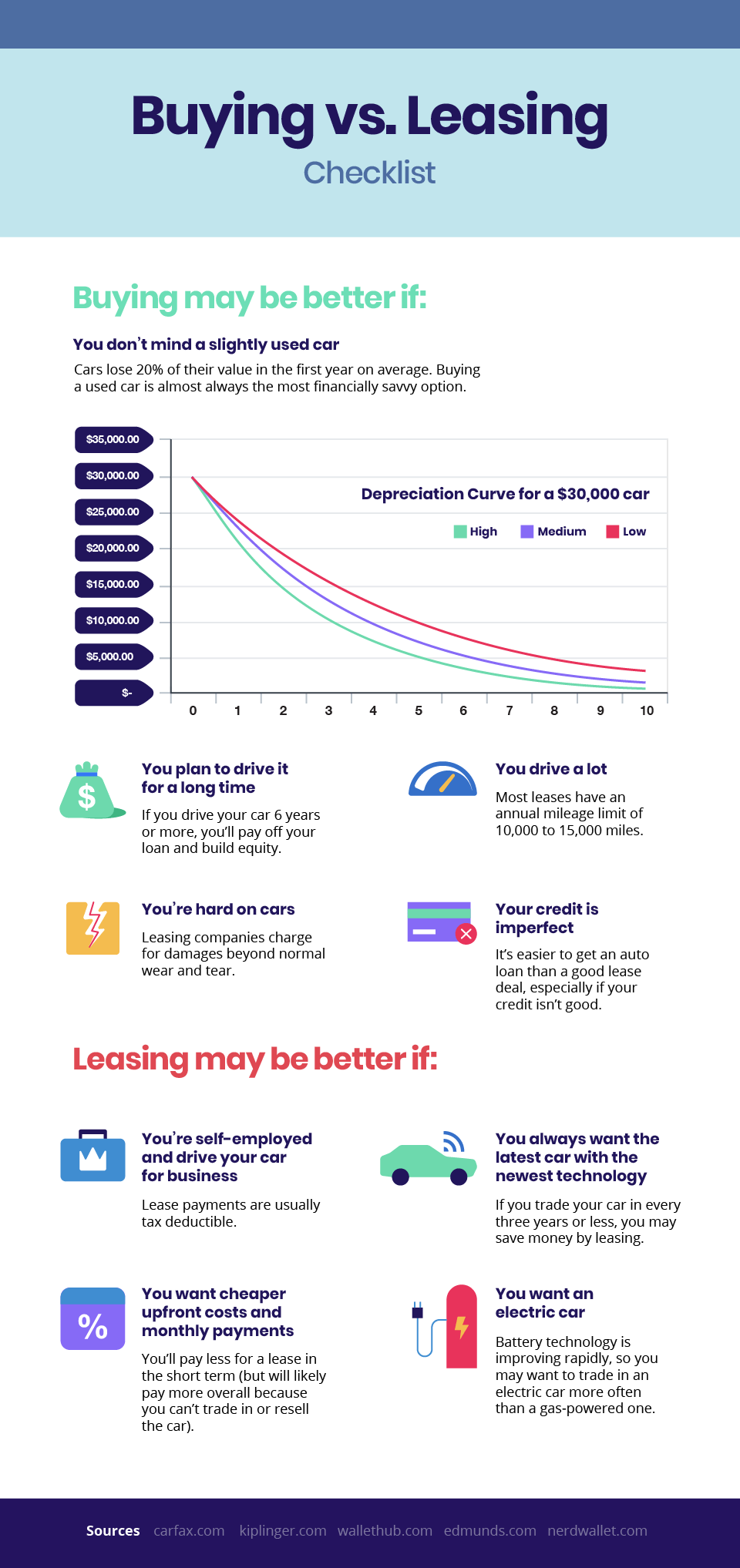

Leasing a car usually requires less expensive upfront costs and monthly payments compared to buying, but purchasing a vehicle is generally cheaper in the long run. Each option has benefits depending on your situation. Buying is probably the better option if any of the following are true for you.

- You don’t mind a slightly used car.

Usually, purchasing a pre-owned vehicle is the most financially savvy decision. That’s because you avoid steep first-year depreciation. On average, a new car loses 10 percent of its value when you drive it away from the dealer and 10 percent more during the next year. A new car loses an average of 60 percent of its total value during the first five years.

Moreover, car insurance and vehicle registration fees are also usually lower for slightly used cars. (However, maintenance and repair costs may be higher.) If you can buy a pre-owned car with cash, you’ll skip interest payments and come out even further ahead financially.

- You plan to keep your car for a long time.

Most car owners keep new cars for six and a half years. If you plan to keep yours that long, buying is usually the better option, especially if you can pay off the loan during that time and build equity.

- You drive a lot.

Most leasing companies charge 12 to 15 cents for every mile driven over a set limit (usually 10,000 to 15,000 miles per year), which can add up. You can negotiate for a higher mileage limit, but you’ll probably have to pay more for the lease.

- You’re hard on cars.

Buying is usually the way to go if you have young kids or haul heavy machinery in your car. When you return a leased car, a little wear and tear is okay. However, the car needs to be close to its original condition or you’ll be charged for damages. Moreover, you may need to show documentation that you got all the recommended oil changes, tire rotations, and tune-ups.

- Your credit isn’t perfect.

It’s usually easier to get an auto loan than a good lease deal, especially if you’re rebuilding your credit. The median credit score among new lessees was 703 in 2017.

When It’s Better to Lease

Buying isn’t always the better option. You may want to lease your next car if any of the following are true for you.

- You’re self-employed and drive your car for business.

You may be able to deduct your lease payment, prorated according to how much you use the car for business. For example, if your lease payment is $300 a month and you drive your car for business 50 percent of the time, you can deduct $150 a month as a business expense.

There’s one catch though. If the car exceeds a certain value you must subtract an “income inclusion” amount from your deduction. This is an additional amount of income you may have to report if you lease a vehicle or other property for business purposes. You must report the inclusion amount if the fair market value of the leased asset exceeds a certain threshold ($50,000 for a vehicle first leased in 2018.) The inclusion amount differs depending on how long you’ve leased your car and is calculated by finding the dollar amount on a price table from the IRS. For a $60,000 vehicle first leased in 2018, the income inclusion amount would be $30 a month for the first year and increase gradually over the next five years.

Bottom line? Leasing offers tax advantages for self-employed people who drive for work, especially for more expensive cars. Being self-employed, you can also deduct business-related car expenses such as parking fees and tolls, gasoline, oil, insurance, garage rent, registration fees, lease fees, and repairs.

- You always want the latest car with the newest technology.

Financing the entire purchase of a car you keep for less than three years usually doesn’t make financial sense. However, if a car is expected to have higher than average resale value, it may still be worth buying.

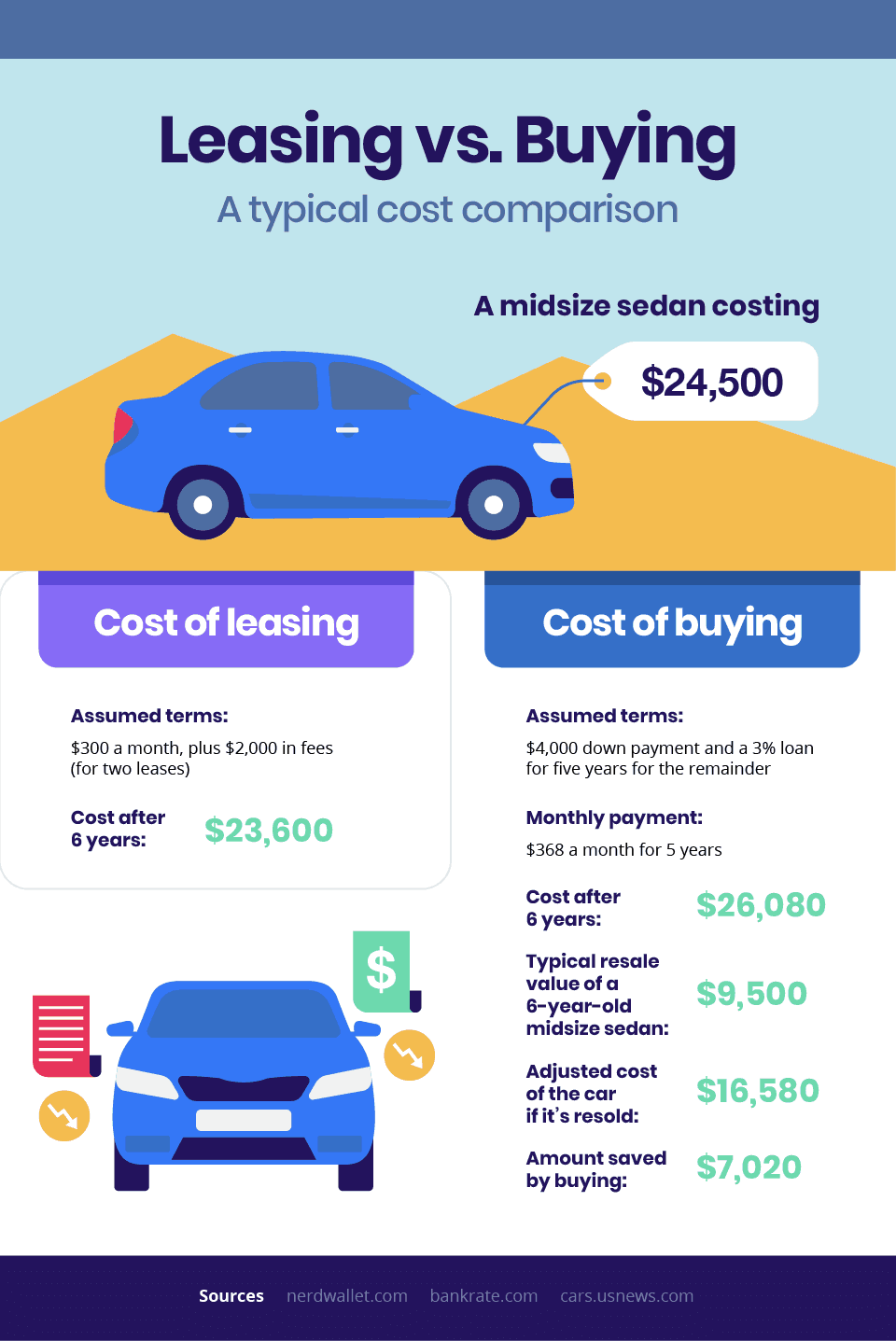

- You want cheaper upfront costs and monthly payments.

When you lease, you only pay for the difference between the sticker price and the car’s expected value at the end of the lease, plus interest and fees. If you have excellent credit, you may not even need a down payment. It’s almost always cheaper in the short term to lease a car rather than buy it.

In one analysis, leasing a new SUV costing $27,142 was about $6,000 less out-of-pocket over six years than buying a similarly priced new car. But remember, at the end of a leasing period, you don’t own the car and can’t resell it. Thus, it’s usually less expensive in the long term to purchase a car.

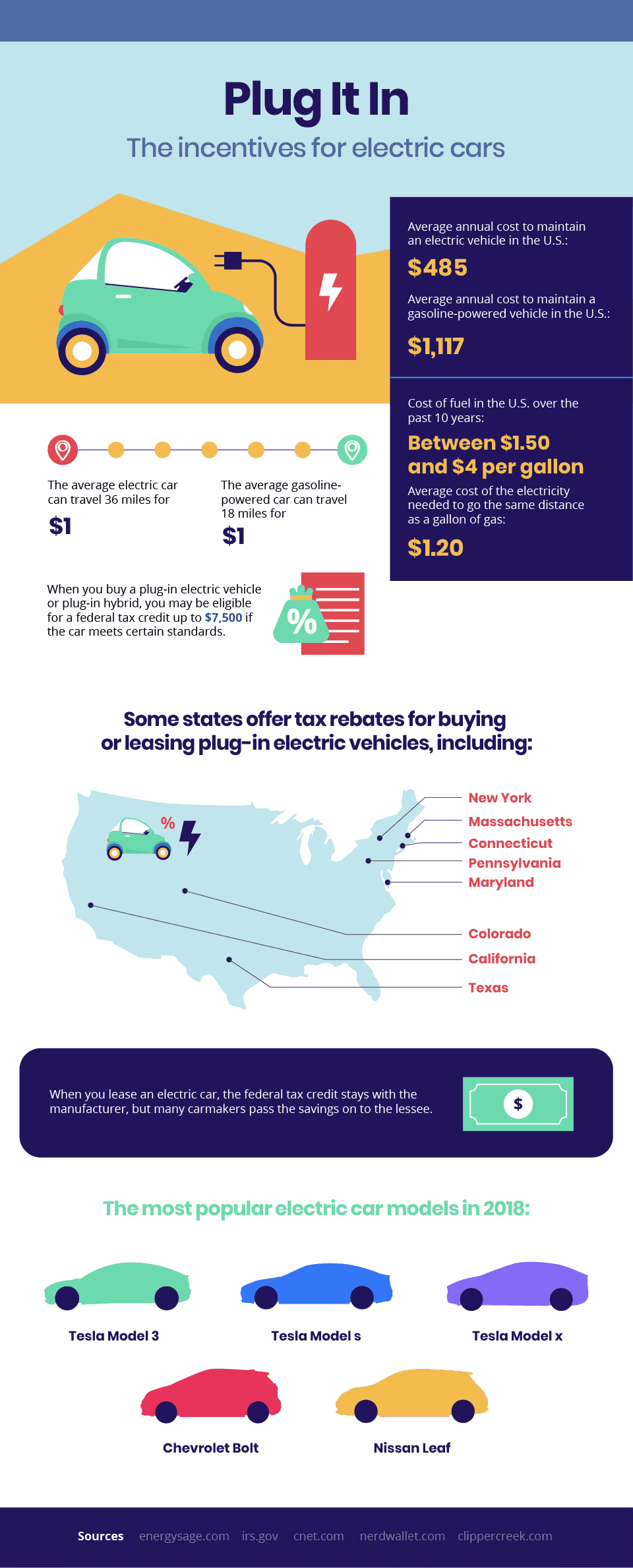

- You want an electric car

There are excellent financial incentives for purchasing a new electric car, including a federal tax credit and rebates in some states. However, 80 percent of electric car drivers lease. Why? First-year depreciation is even steeper for electric cars than for gas-powered cars.

On average, electric cars manufactured in 2016 lost 52 percent of their value during their first year. Moreover, batteries degrade over time, and battery technology is quickly evolving. The electric vehicles manufactured in two to three years will likely have much better range than today’s electric cars.

Conclusion

Before you get behind the wheel of your next new car, it will pay to research the pros and cons of buying versus leasing. Learn about the tax advantages and run cost comparisons before you make a decision. And whether or not you choose to buy or lease, don’t forget to enjoy the ride.

Share this Image On Your Site